You may have heard of FERS deferred retirement – where you separate from service now, but start your FERS pension later. But you might also be eligible for a Postponed FERS Retirement.

If you’re thinking about leaving federal service – it’s important to understand your options *before* you leave.

In the FERS Pre-retirement classes I teach, many people have heard of FERS Deferred Retirement. And a few people have heard of FERS Postponed Retirement.

But very rarely have I had someone who understood the *BIG* difference between the Deferred and Postponed Retirement.

Let’s talk about the difference between FERS Deferred Retirement and FERS Postponed Retirement. Then you’ll be able to click on a link that will take you to another page that has more details and examples about each one.

But first, what is that *BIG* difference?

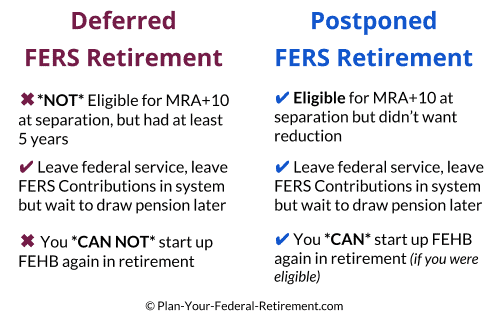

The *BIG* Difference?

FEHB. Your Federal Employee Health Benefits.

With a Deferred FERS Retirement, you can start your FERS pension back up later – but you can’t start FEHB again.

With a Postponed FERS Retirement – if you were eligible to keep FEHB when you separated from service – you can resume your FEHB coverage when you start your pension.

Why is this such a big deal?

As a federal employee, you have a phenomenal benefits package. Of all of the benefits you have as a federal employee… I believe that your *biggest* benefit is your ability to keep FEHB into retirement.

But you can only keep FEHB in retirement if you meet certain requirements. And if you do a FERS Deferred Retirement – you can’t keep it at all.

What makes the difference between a Deferred and Postponed Retirement?

The difference has to do with whether or not you were eligible to take an immediate MRA+10 retirement before you separated from service.

If you were *not* eligible for MRA+10 when you left – you can not do a Postponed Retirement – only a FERS Deferred Retirement (assuming you meet those qualifications as well).

If you *were* eligible to do an immediate MRA+10 retirement when you left – you *can* do a Postponed Retirement.

Here’s a quick summary…

Let’s go over the basics of FERS Deferred Retirement and FERS Postponed Retirement…

Basics of FERS Deferred Retirement

To do a FERS Deferred Retirement… you must..

- Have at least 5 years of creditable civilian service before you separate

- AND you must leave your contributions in the FERS system

Basically – you leave federal service now. You leave your contributions in the system. Later, when you reach a specific age (usually 62) you can start your pension.

With a FERS Deferred Retirement, there is no minimum age to reach before you leave service – but you must wait until a specific age to start your pension.

Click here to learn more about FERS Deferred Retirement, including sample pension calculations.

Basics of a FERS Postponed Retirement

To do a Postponed FERS Retirement – you must …

- Have reached your MRA before you separate

- Have at least 10 years of creditable service

Do you know your MRA? Your FERS MRA or Minimum Retirement Age is a number that plays into your eligibility for different types of FERS retirement. MRA is between 55 and 57 depending on when you were born.

When you do a Postponed Retirement – you had the option to do an MRA+10 Early Retirement when you left federal service. But instead of taking a reduced pension, you wait until you reach a specific age (usually 62) to start your full pension.

And if you were eligible to keep your FEHB when you separated from service – you can resume your FEHB coverage and keep it in retirement.

Examples of FERS Deferred Retirement vs. Postponed Retirement

Let’s look at an example of doing a FERS Deferred Retirement and an example of a FERS Postponed Retirement.

For our example, we’ll use Jane. Jane’s MRA is 56. Jane is 55 years old now, and she has 9 years of creditable service. For easy numbers, we’ll say her High-3 Salary is $100,000.

Jane wants to leave federal service and take a job in the private sector.

She’s trying to figure out whether she should leave now (and do a FERS Deferred Retirement) or work another year so she can do a Postponed Retirement.

Let’s take a look…