How will your pension be taxed in retirement as a Federal Employee?

We love talking about retirement but nothing gets us out of bed faster than the opportunity to talk about retirement AND taxes! Seriously, talking about retirement tax strategies is one of our favorite subjects.

In this article, we are going to go through Glynn’s question about how much of his pension will be taxed in retirement. As a federal employee, you have probably heard before that the portion of your pension you contribute to while working will not be taxed in retirement. Under the Federal Employee Retirement System (FERS) your contributions are only a portion of your pension. The rest is made up by your employer, the Federal Government.

What does this mean to you as a potential retiree? Let’s dive in and look at an example using what Glynn, a federal employee under FERS, has provided.

Certified Summary of Federal Service

About a year prior to when you plan to retire, we encourage you to request a Certified Summary of Federal Service from your Human Resource office.

Note: a Federal Benefits Estimate is NOT Certified Summary of Federal Service. The keyword in Federal Benefits Estimate is ESTIMATE. It’s your HR’s best guess at what your benefits will be when you retire. It’s a great place to start getting an idea but should NOT be counted on as an official calculation of your retirement benefits. Only a Certified Summary of Federal Service can provide you with this information. A Certified Summary of Federal Service audits your entire official personnel file and determines eligibility for all years worked. By reviewing your Certified Summary of Federal Service BEFORE you apply for retirement, you have an opportunity to review and make corrections with your Human Resources department while you are actively working.

Applying for Retirement under FERS

When you are ready to apply for retirement under FERS, you will complete the Application for Immediate Retirement (SF-3107).

The application for immediate retirement is the form that you will use to make what reductions you want placed on your pension.

Note: OPM calls your pension an annuity. In the world of finance, annuities mean something else so we call yours what it is – a pension.

The decisions that you make on your Application for Immediate Retirement are often irreversible particularly after the first 12 months of retirement. Read the form carefully and choose wisely. If you need help completing an Application for Immediate Retirement, consider contacting our office to schedule an appointment with one of our Financial Advisors.

On your Application for Immediate Retirement, you elect what reductions to your pension you want.

Survivor Benefits for Spouse,

Survivor Benefits for Dependent Children,

Life Insurance Benefits and,

Health Insurance Benefits.

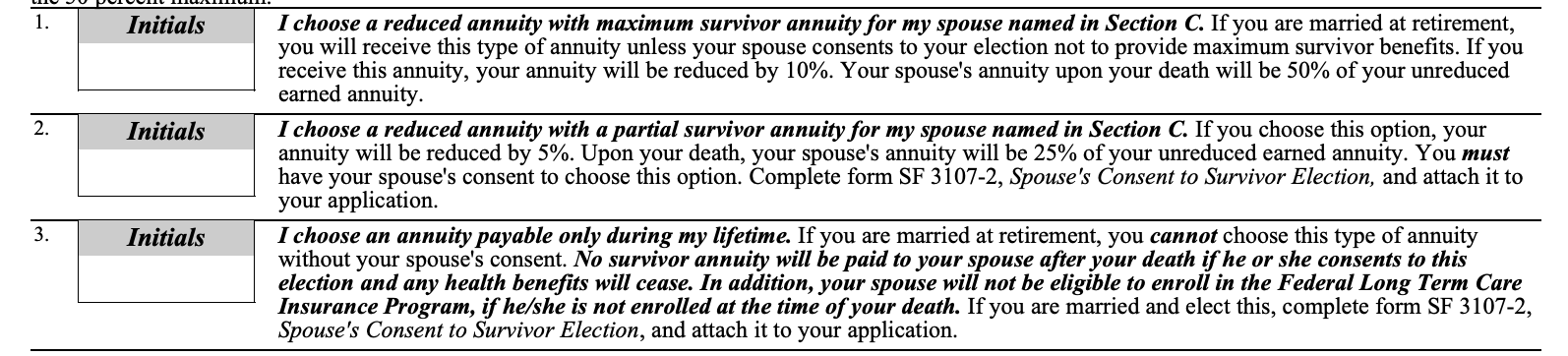

Of particular importance are your survivor benefit options,

If you choose to leave your spouse the full survivor benefits, as Glynn is in our example, your pension will be reduced by 10%.

Glynn’s example:

$3,000.00 Gross Monthly Pension

-$300.00 Survivor Benefits at 10% of his pension

$2,700.00

Your survivor benefits are a pre-tax reduction from your pension.

Your contributions to your pension are also pre-tax. This amount is rather insignificant so we encourage you not to get too caught up in thinking that it makes up a substantial part of your non-taxable income.

However, life and health insurance elections are not pre-tax. This is a big difference between when you are working as a federal employee and when you retire.

When you are working with the federal government your health insurance premiums and life insurance premiums are deducted from your paycheck pre-tax. When you retire, they are post tax.

As a Federal employee, tax planning for retirement is a critical component of your financial plan and an ongoing one. It is one of the most disproved theories that we hear from federal employees, “when I retire, my taxes will be lower and not matter as much.” Remember, under FERS a significant number of your benefits are subject to federal income taxes: your FERS Pension, your traditional TSP and Social Security.

If you have questions, like Glynn’s, make sure you let us know. We love diving into your benefits and answering questions about how your Federal Employee benefits work and what considerations you need to make to your greater financial plan because you are a Federal Employee.