Hello Tammy and Micah, Great podcast! Learning a lot. About 5 years away for earliest retirement date. Question: let’s pretend money is NOT an issue for retirement due to FERS Pension, SSA, TSP, Investments but will need FEHB. For estate planning, do you have any thoughts on getting full spousal annuity 50% knowing that this is not transferrable to trust/children OR 25% spousal annuity and where would you recommend to invest which could be used for spouse or go into trust for family. Both sides of family live into 80s and we are in our early 50s currently. Interested in your advice or how to best decide. Cordially, Gene

Remember that your income will change when “two of you” becomes “one of you.”

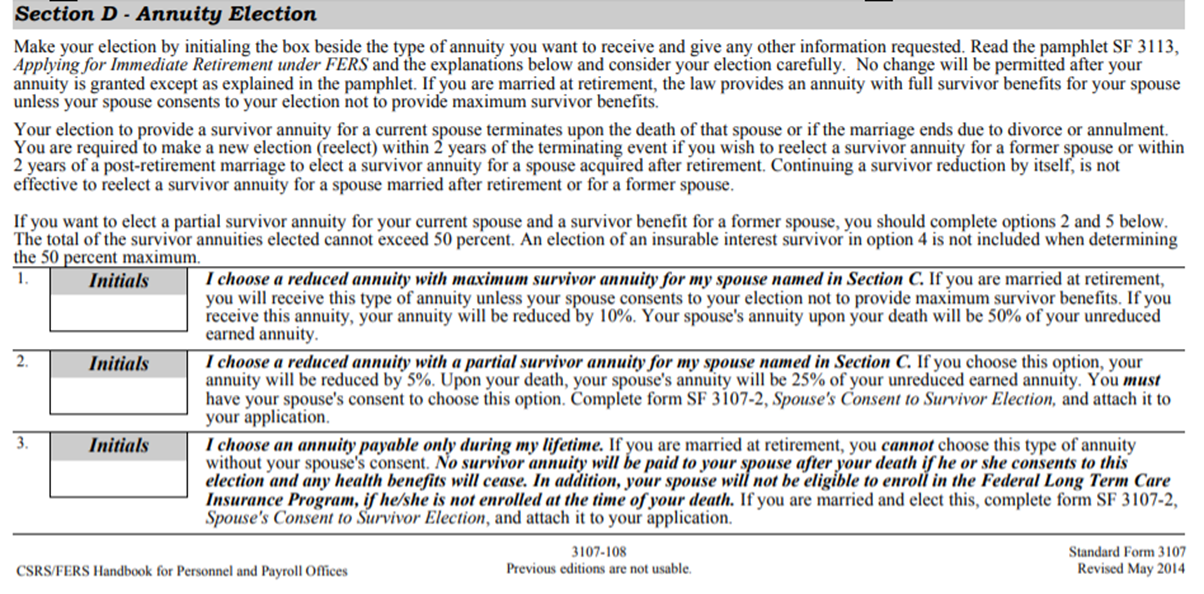

You may have sufficient retirement income while you and your spouse are both living. Consider federal retirement benefits under FERS (or CSRS), other retirement benefits that may be payable (i.e. military retirement, private sector pension or state or local pension benefit), Social Security benefits (earned and/or spousal benefits), and retirement savings in the TSP, IRAs or other retirement savings program. Have you figured out how this will change when one spouse passes away? The surviving spouse will receive a widow’s benefit or their own earned benefit, whichever is higher. In addition, retirement savings may be depleted depending on factors related to retirement spending and the ability for the account to continue to grow during retirement. If there is no survivor election under FERS, the surviving spouse can lose another valuable source of income and with no survivor benefit, they can also lose coverage under FEHB.

FERS Retirement (Unreduced) | Maximum Survivor Benefit Reduction | Reduced Benefit |

$30,000 | $3,000 | $27,000 |

Partial Survivor Benefit Reduction | ||

$1,500 | $28,500 | |

Spouse Predeceases Annuitant | Maximum Surviving Spouse Benefit |

$30,000 | $15,000 |

Partial Surviving Spouse Benefit | |

$7,500 |

Key Points To Remember!

- Cost of election reduces your taxable income.

- Survivor benefit is adjusted by cost of living adjustments before and after the retiree dies.

- This is a permanent election and protects the spouse should they become widowed.

- The survivor benefit is payable for the life of the surviving spouse.

- If your spouse predeceases you, your unreduced FERS retirement is restored.