Immediate Retirement

“An immediate retirement benefit is one that starts within 30 days from the date you stop working. If you meet one of the following sets of age and service requirements, you are entitled to an immediate retirement benefit:

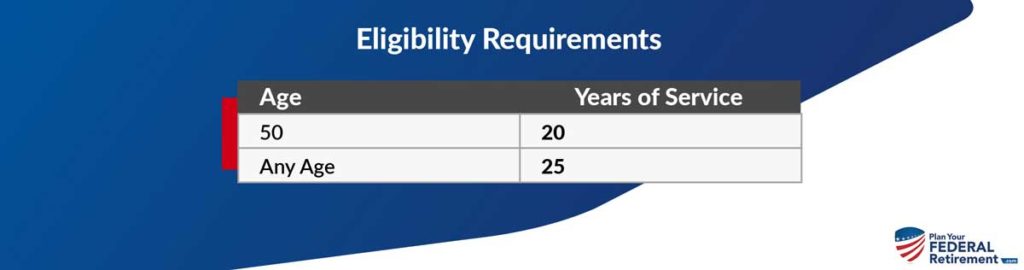

| Age | Years of Service |

|---|---|

| 62 | 5 |

| 60 | 20 |

| MRA | 30 |

| MRA | 10 |

If you retire at the MRA with at least 10, but less than 30 years of service, your benefit will be reduced by 5 percent a year for each year you are under 62, unless you have 20 years of service and your benefit starts when you reach age 60 or later.

Early Retirement

The early retirement benefit is available in certain involuntary separation cases and in cases of voluntary separations during a major reorganization or reduction in force. To be eligible, you must meet the following requirements:

That all seems rather straight forward. You need to meet the age and service criteria to be eligible to retire.

But what about the exceptions? If you are considering retiring from FERS before you meet a certain age and time in the service parameter outlined above?

Assuming that you are not filing a Disability Retirement, which is another beast in and of itself, you have two choices to leave Federal Service before being eligible for an immediate annuity: Postpone your retirement or defer your retirement. ” (opm.gov)

They sound like a similar concept but they are totally two different animals.

FERS Bonus Retirement

When you meet the rules of eligibility for receiving a FERS pension (which OPM calls an “annuity”) your pension calculation is based on your Hi-Three and credible service using a 1% multiple.

But what about this FERS Bonus? What some Feds call the “FERS Bonus Retirement” which is what Katherine is referring to, is an extra 10% in retirement income because the multiple that OPM will use to calculate your retirement is 1.1%

Here is how.

If you retire at age 62 with at least 20 years of Federal Service you get a special retirement calculation for your pension – the FERS Bonus Retirement.

Note the requirements for the FERS Bonus: age 62 and with at least 20 years of creditble service.

Not age 61 and 10 months.

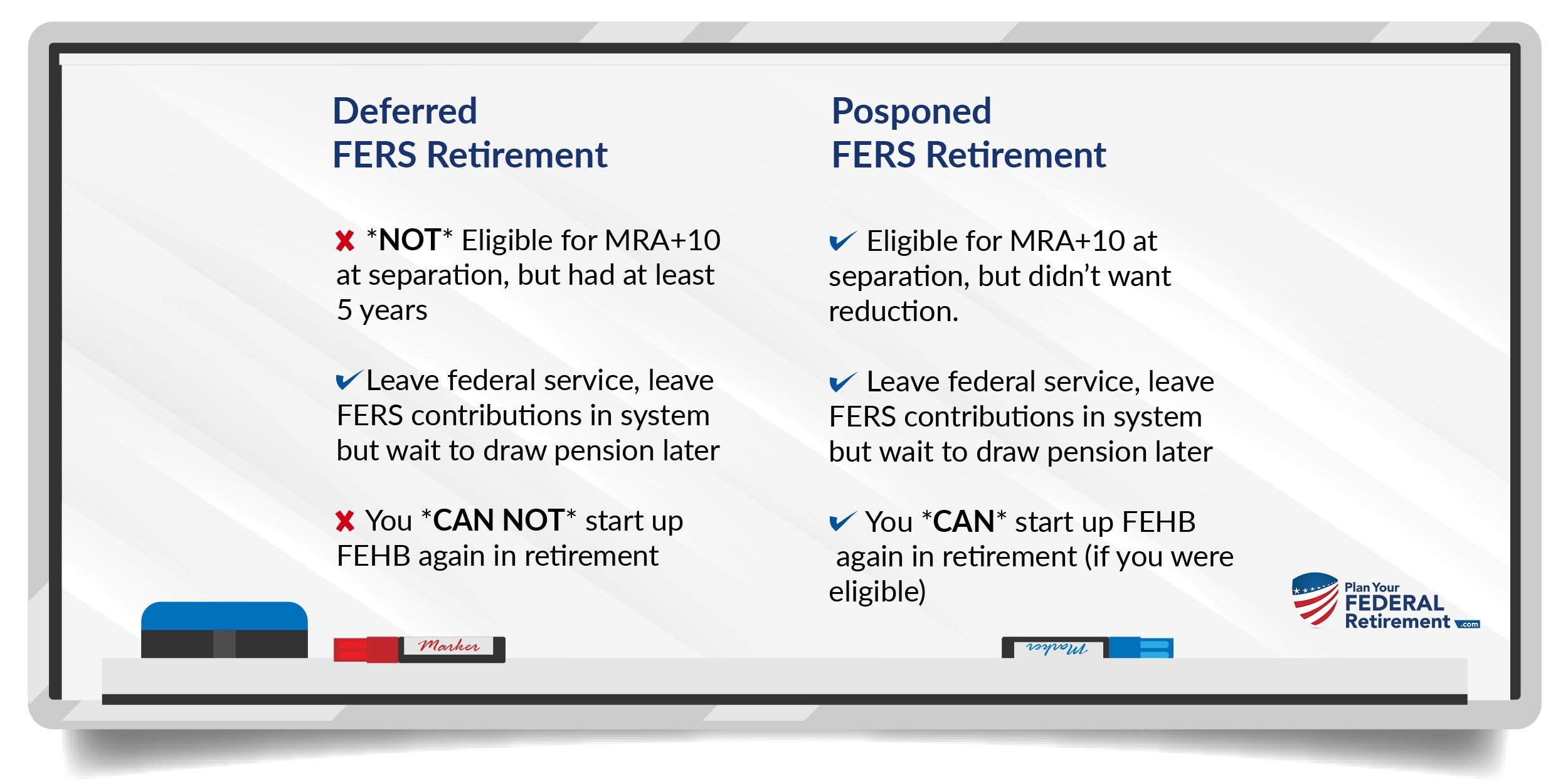

At age 61 and 10 months, Katherine elected to separate from Federal Service and chose to do so under a postponed retirement.

Post-Poned vs. Deferred Retirement

We go into the big differences between a postponed vs. a deferred retirement system here.

We will skim over the topic here just so that you can understand what choices that Katherine was making at the time but won’t go into it otherwise so that we can get into Katherine’s question more extensively.

Katherine chose to postpone her retirement because she had met her Minimum Retirement Age, had more than 10 years of creditable service and wanted to be able to leave Federal Service and resume Federal Employee Health Benefits (FEHB) in retirement.

When Katherine hired her “retirement consultant” who was a former HR person, she asked if there was anything that she should consider by leaving service at 61 and 10 months.

What a great time to mention that if Katherine were to work another 2 months she would qualify for the FERS Retirement Bonus calculation.

Katherine estimates that she lost out on $400 a month, which is $4,800 a year. If Katherine you are currently age 63 and you have a normal life expectancy of say… 88 years of age that is… well, let’s just stop here.

Not sure the math on this would make you feel any better. Instead, let’s look at solutions.

Solutions

Now we understand the costly mistake that bad advice on a FERS Postponed retirement caused so what options does Katherine have?

Well, Katherine, you could consider looking at getting rehired for a few months in any federal full-time position. I know that doesn’t sound ideal but if you are missing a few months, could going through the hassle of getting rehired be worth it?

We have not had clients do this before but it is an option that you could explore.

As for attorneys in this subject matter, we don’t have a specific point of contact that would be helpful regrettably.

As for recourse with the retirement counselor, I am not certain that a former HR Person has any fiduciary responsibility when they provide advice because they are skirting just outside the realm of providing financial advice normally.

We really wish that we could provide you, Katherine, with solid advice on how to rectify this situation but aside from seeing if you are eligible to resume employment under Federal Service we just aren’t sure what else can be done to provide you with the clear way to rectify having missed out on the FERS Retirement Bonus when you elected a postponed retirement.

Read through our 7 Retirement Mistakes to know what problems you might encounter and how to solve them.

Questions

If you have questions about your Federal Employee Benefits, please let us know. When you submit your question you might be featured on FERS Federal Fact Check where we help Federal Employees understand more about their FERS Benefits.

JC Shilanski