FERS Retirement with 10% Bonus:

Higher Pension for Age 62 & 20 Years

Some people who qualify for regular FERS retirement will also qualify for a special 10% bonus. If you retire with at age 62 (or older) and with at least 20 years of creditable service – your pension gets a 10% bonus.

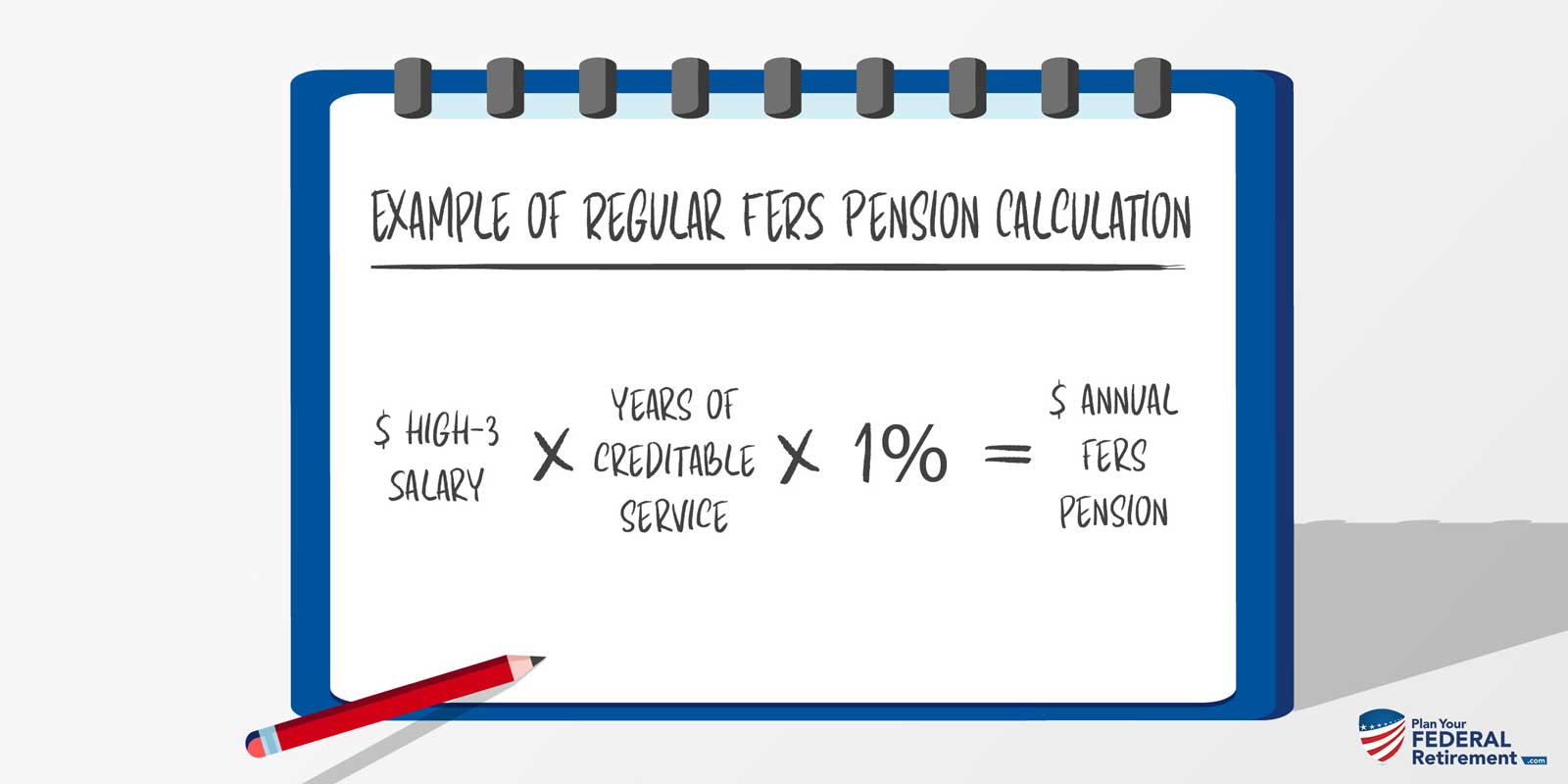

Your FERS retirement pension is determined by your High-3 salary, your years of service and a pension multiplier.

For most FERS, that pension multiplier is 1%. So their pension comes together as…

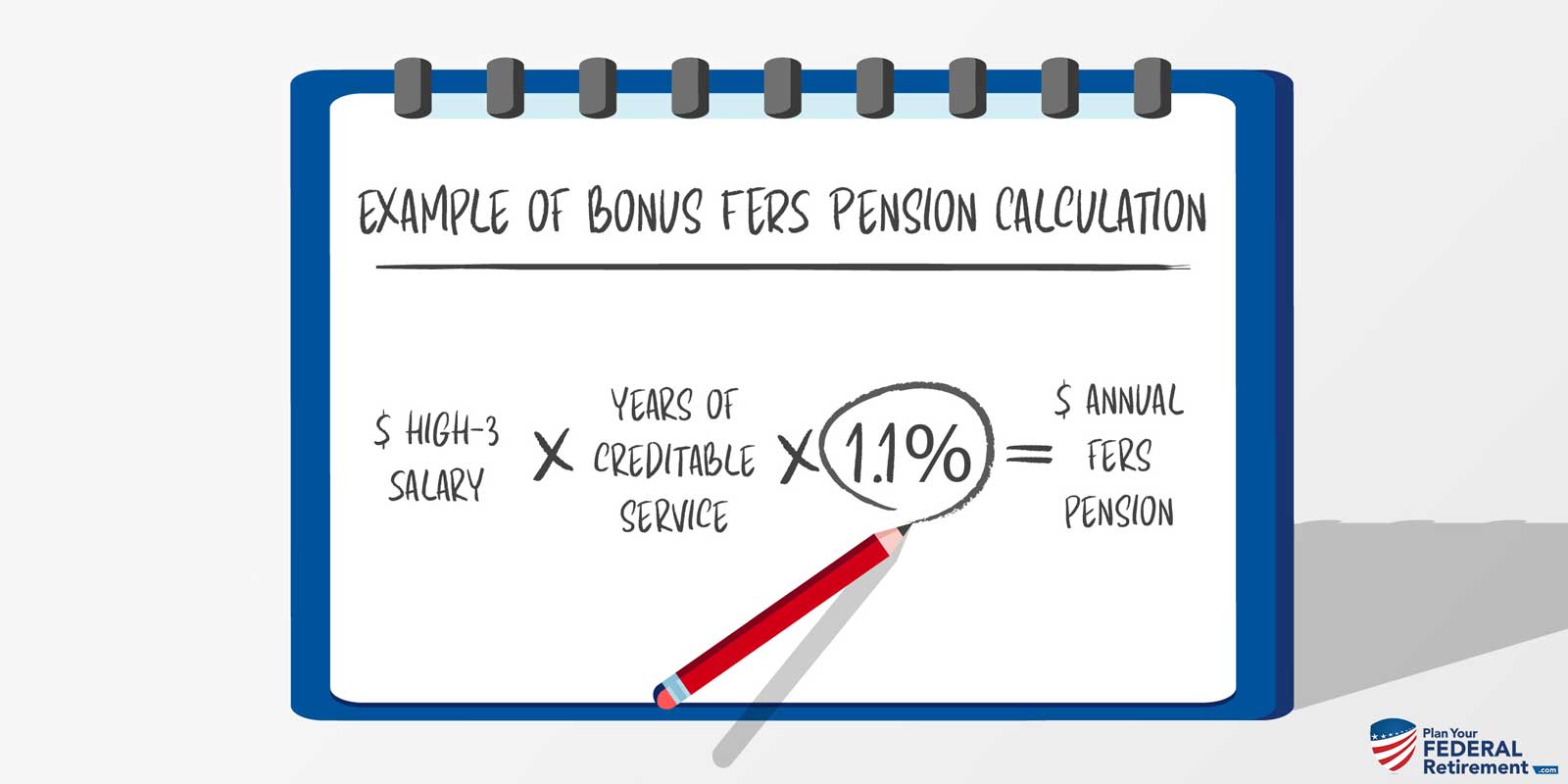

But if you retire at age 62 or older with 20 or more years of creditable service, your pension multiplier is 1.1%

That’s a 10 percent bonus! And you’ll get the benefit of that bonus for the rest of your life.

Special Rules for the 10% Bonus

In order to get the bonus, you must be at least 62 years old at retirement with at least 20 years of creditable service.

You must also be going out on an immediate FERS Retirement. This means that if you were doing a Postponed FERS Retirement – you would not be eligible for this bonus.

Also, this bonus doesn’t apply for Special Provisions who have a different pension multiplier.

For more details about the bonus, you can check out Chapter 50 of OPM’s CSRS / FERS Handbook This bonus is mentioned in Section 50B3.1-1 Subsection B.

When people read that section, sometimes they become alarmed when they see “NOTE 2: Employees who are age 62 at retirement are not eligible for a retiree annuity supplement.” We’ll talk more about that in a moment.

Are you considering sticking around to get the 10% bonus? Let’s go over some important considerations…

“Should I Stay or Should I Go?”

Are you eligible to retire now under regular FERS Retirement rules, but you’re trying to decide if you should stay to get the 10% bonus?

Everyone’s personal situation is unique. But let’s look at some examples that might help you evaluate your own situation.

Let’s say you’re 61 with 20 years of service. That means that you’re eligible to retire now under regular FERS retirement rules.

But you’re wondering if it makes sense to work one more year so you’ll be 62 when you retire and qualify for the bonus…

Let’s take a look at some sample pension calculations to see how much of a difference the extra bonus really makes in your FERS retirement.

Sample FERS Pension Calculations…

With and Without the 10% Bonus

First – let’s go over the example we use for regular FERS retirement pension calculation:

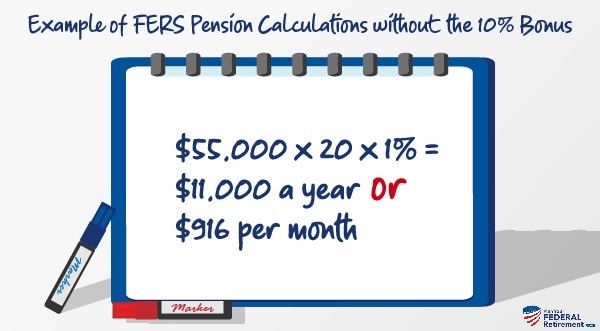

We have someone with a High-3 of $55,000, and they have 20 years of service. If they are not yet age 62 when they retire, their pension will be calculated as…

But what if you had someone with the same High-3 and same years of service – but they were at least age 62 at retirement.

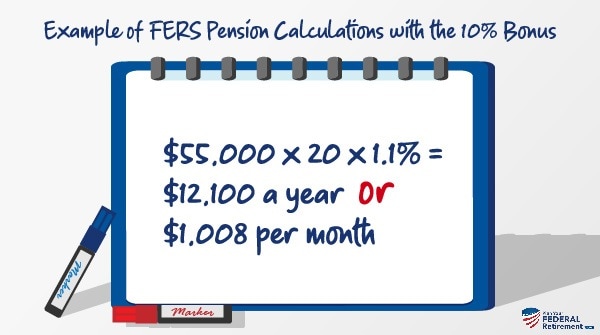

Their FERS Retirement pension would be calculated as…

In these examples, we kept the years of service the same to show the effect of the bonus. And the difference here amounts to ($1,008 – $916) $92 more a month.

Sure that sounds nice – but in the real world, the difference is often quite a bit more.

…But In the Real World…

If you’re trying to decide to punch out now, or wait another year – there is more to consider.

If you work another year – you have several things going for you that can increase your pension even more than 10%.

- You’ll have one more year of creditable service – and this will make your pension higher.

- And odds are that your High-3 will be a bit higher as well.

Let’s take another look at our example and see how these changes impact the difference…

Let’s go back to the first part of the example where we say you’re 61 with 20 years of service and a High-3 of $55,000.

Again – your FERS Retirement pension would be…

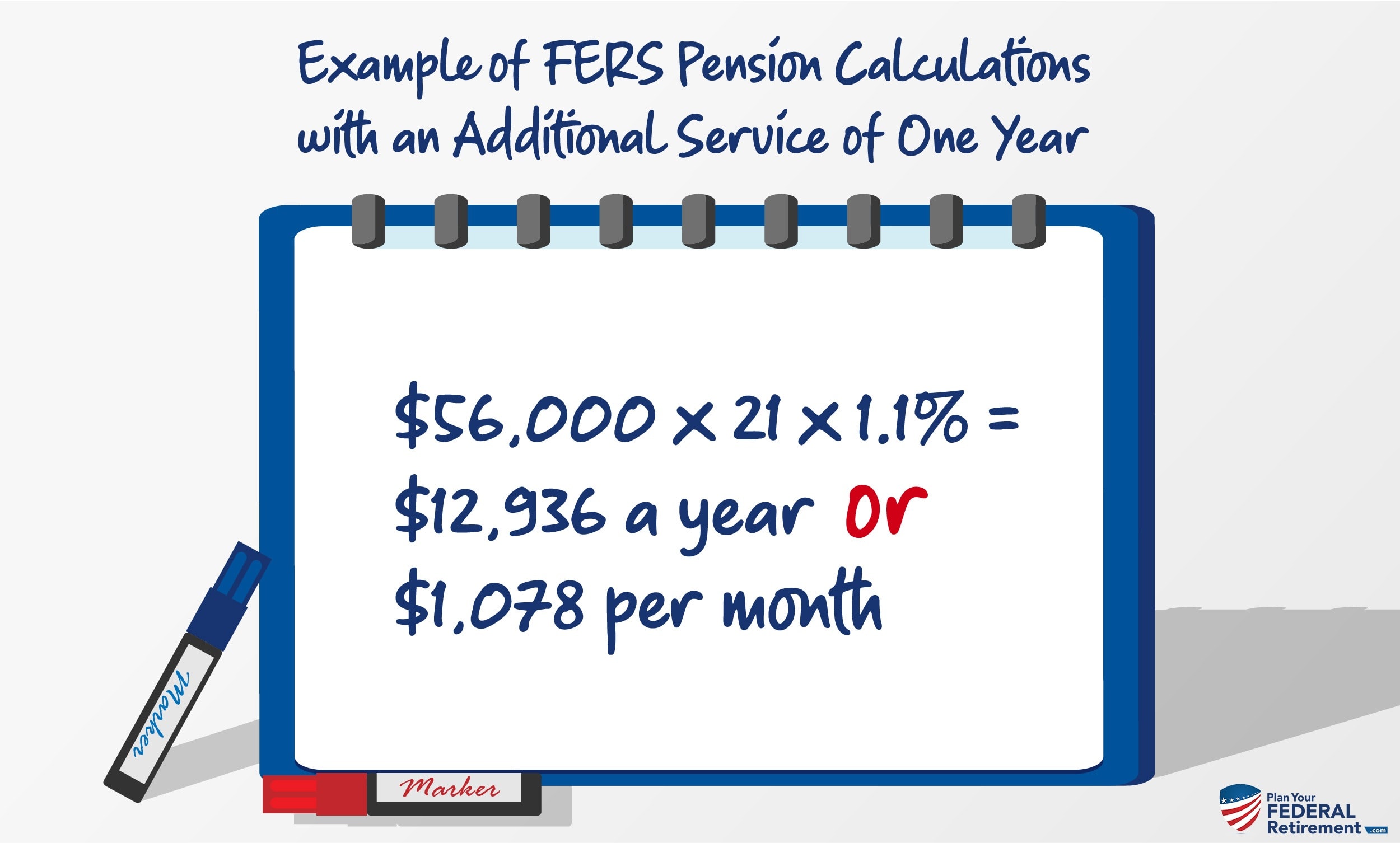

However, if you worked another year, and instead retired at 62, with 21 years of service and a High-3 of $56,000 – your FERS Retirement pension would now be calculated as…

Now the difference here amounts to ($1,078 – $916) $162 more a month.

And not only will you benefit from that higher pension for the rest of your life… if you do a survivor annuity, your survivor’s benefit is based on that higher amount for the rest of their life as well.

Example of Difference for FERS Survivor Annuity

Looking at our example, if you retire at age 61 with 20 years of service, your gross monthly pension was $916.

In this case, if choose the ‘full’ survivor annuity (which means your survivor gets *half* of your pension when you pass away) – it will cost 10% or $91.60 – and your survivor would receive $458/month.

However, if you work another year and go out at age 62 with 21 years of service, your gross monthly pension would be $1,078.

Now, if you choose the ‘full’ survivor benefit (where they receive half)… it will still cost 10% – which is now $108 – but your survivor would receive $539/month.

So by working that extra year – your gross pension was ($1,078 – $916) $162 higher each month of your life. And when you pass away your survivor’s benefit will be ($539 – $458) $81 higher each month for the rest of their life.

Please keep in mind that we’re just talking about gross pension numbers here. The actual FERS Retirement pension you receive will be reduced by survivor benefits, FEHB, taxes, etc. But we’re just talking gross numbers to cover the concept.

“But I’ll Lose the FERS Supplement”

In the FERS pre-retirement classes I teach – we talk about the 10% bonus.

One concern people bring up is that if they wait to retire at age 62, they ‘lose’ the FERS supplement.

And yes, that is correct. If you retire at age 62 or after, you do not get the FERS Supplement.

But let’s continue our example to see how big of a difference this really makes.

Let’s continue our example…

Let’s say your FERS Supplement would be $500/month if you retired at age 61.

So if you retire at age 61, you’d be getting your pension of $916/month and the supplement of $500/month. $916 + $500 = $1,416/month.

And technically that is higher than the pension of $1,078/month you’d receive if you worked another year to get the bonus and forgo the FERS Supplement.

*BUT* keep in mind, you would only get the Supplement for a year, because the FERS supplement stops at age 62. And it doesn’t matter if you have started Social Security or not – the FERS Supplement automatically stops at age 62.

If you work longer to get the 10% bonus – you get the benefit of that bonus for the rest of your life. And if you choose a survivor annuity – their benefits will be higher as well.

Also, let’s not forget that if you work another year – that was another year you received your full salary.

So if you worked another year until age 62 – yes – you would be giving up the FERS Retirement Supplement of $6,000 – but you’d be getting your full salary of roughly $56,000 in this case … AND you’d get a higher pension calculation for the rest of your life.