“I am 59 and planning to retire a year from now. My wife will retire at the same time (but at age 61, not a federal employee). We are planning to take her Soc Sec at age 62 and wait with mine till age 70. I have about 2/3 of my TSP in traditional and 1/3 is Roth. My question is, if I am planning to supplement my living expenses from my TSP, prior to collecting Soc Security, would I be better off taking it out of the Traditional or the Roth balance?” – Randolph

As a Federal employee, you 100% understand your income during your working years. You know that every two weeks, 26 times a year, that you will receive a direct deposit paycheck. Unless there is a furlough. 🙂

Knowing what your net income is going to be month to month allows us to cash flow our expenses and anticipate our needs better.

When you retire as a Federal employee, your income sources and schedules will change. There will be a lot of moving parts and not all of them will happen simultaneously.

Income sources for retirees under FERS:

Age | Income Type | Note |

MRA | Pension | Your Hi-Three X Years of Service X1% (in most cases). Received MONTHLY, not every two weeks. |

55 | Thrift Savings Plan | If you separated from service as a retiree, you’re able to access the TSP without the 10% penalty. |

57 – 62 | FERS Special Supplement | If eligible to receive. |

59 ½ | Thrift Savings Plan | Eligible for penalty free withdrawal if still working. |

62 | Social Security | First eligible for a REDUCED social security amount. |

65 | Medicare | Eligible to enroll. |

Full Retirement Age (maybe age 67) | Social Security | Your full social security benefits. |

70 | Social Security | Your MAXIMIZED social security benefits. |

72 | Thrift Savings Plan | Required Minimum Distributions under the Secure Act. |

You probably thought that when you retired, your life would be less complicated!

One of the questions that we work with our Federal Employee clients alot about is when to start and stop these income sources.

Randolph asks this indirectly when questioning when he and his wife should start social security and when to use their Thrift Savings Plan (TSP) to fill any potential gaps between the income they will receive in retirement and the lifestyle they want.

FERS Pension and FERS Special Supplement

FERS Eligibility to Retire

Eligibility Information to Retire under FERS with an Immediate Pension:

Eligibility Information to Retire under FERS with an Immediate Pension:

Age Years of Service

62 5

60 20

MRA 30

MRA 10

Reduced Pensions: if you do not meet the above criteria you may be eligible for retirement under FERS under a reduced pension. If you retire at the MRA with at least 10, but less than 30 years of service, your benefit will be reduced by 5 percent a year for each year you are under 62, unless you have 20 years of service and your benefit starts when you reach age 60 or later.

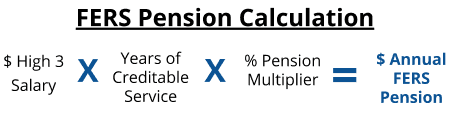

FERS Retirement Calculation

Your Gross FERS pension (before taxes and other elective reductions) is calculated based on three components:

- Your High-3 Salary

- Years of Creditable Service

- Pension Multiplier

FERS Special Retirement Supplement

As you can see under the rules of eligibility, some Federal Employees are eligible to retire before they are eligible to receive social security benefits.

That is why the Special Retirement Supplement was put into effect. The Special Retirement Supplement fills the gap between when a FERS employee is eligible to retire for a full unreduced pension (providing they’re under age 62) and when they first becomes eligible to receive social security benefits at age 62.

Just because a person is eligible for social security benefits does not mean that they should begin them at age 62.

In order to be eligible for the Special Retirement Supplement, you have to retire under one of the following rules:

- Retire at your MRA with 30 or more years of creditable service

- Retire at age 60 or older with 20 or more years of creditable service

- Retire with Special Provisions (such as a firefighter, LEO, air traffic controller, and more) and be either 50 years old, or have 25 years of service.

The eligibility is the same as qualifying for an immediate pension; therefore, an early retirement (retire at MRA or older with at least 10 years of creditable service) does NOT qualify for a Special Retirement Supplement.

The Special Retirement Supplement is calculated for you by OPM. They use a formula involving your earnings history to calculate your benefit computation years, which they then use Social Security law to finally arrive at your SRS pension amount.

A much simpler way of finding how much your Special Retirement Supplement would be is by using the estimated Special Retirement Supplement formula, shown below:

(Years of Creditable Service / 40) x Your Age 62 Social Security Benefit

Your Special Retirement Supplement is almost always lower than what your gross Social Security benefit will be. That is because the formula that OPM uses to calculate your Special Retirement Supplement does not begin accruing until age 21 for Actual Pay. Many people began working before age 21.

Your Special Retirement Supplement, if you receive one, will automatically stop when you reach age 62. Trust us, the Federal Government is pretty good and stopping this without you mentioning anything, they know when you’re 62 and this benefit should end.

Should you start social security at age 62 once your Special Retirement Supplement stops?

Age 62 – Reduced Benefits

You are eligible at age 62 to begin drawing your social security benefits. However, at a permanent reduction. That permanent reduction in your social security benefits can be up to a maximum of 30%.

For the rest of your life.

The rest of your life… that’s a long time for a permanent reduction. If you are eligible at retirement for a Special Retirement Supplement that benefit stops at age 62. This is when most Federal Employees that we talk with, think that they need to start social security.

One benefit stopped, now they need to start the next. You may have other choices though that could be more beneficial to your long term financial plan.

Full Retirement Age (FRA)

At your FRA you are eligible to receive 100% of your benefits from social security.

If you are unsure of what your benefits will be or what your FRA is, you can check! We encourage you to log onto your personal account at ssa.gov to find out.

Your most recent social security statement will show you your FRA, earnings history and estimated benefits amount at FRA.

Age 70 – Delayed Social Security Benefits

The maximum age that you can delay taking your social security benefits is age 70.

For every year beyond your FRA that you delayed taking benefits from social security, you received an 8% increase.

Contingent on your FRA, you could delay your benefits until age 70 and receive 132% of your benefits.

![]()

Withdrawals in Retirement from Traditional and ROTH TSP

As a Federal employee, your third potential “income” option is your Thrift Savings Plan (TSP). During your working years, you and your employer contributed to your TSP. You made investment decisions based on your objectives for retirement and intend, or most likely intend, to use these funds to supplement your retirement and keep up with inflation.

When you retire from Federal Service you should be receiving your pension and potentially a Special Retirement Supplement which stops at age 62 when you are first eligible for social security benefits.

If you plan to delay drawing from social security benefits until you reach your Full Retirement Age or, age 70 to receive the absolute maximum retirement benefits from social security – you may need / want to withdraw funds from your TSP to do so.

This is what our example, Randolph is considering especially because in his case, he and his wife are of different ages and have different working histories.

Randolph has been contributing to both his Traditional TSP and the ROTH TSP. He wants to know which of these “sleeves” he should take money from in order to supplement his retirement income needs while they wait to maximize social security.

Under the TSP Modernization Act, you can now choose which “sleeve” you want to take your funds from: the Traditional TSP or the ROTH TSP.

However, there are still ROTH Rules that Randolph needs to consider. In order to take a distribution from your ROTH TSP without penalty or forfeiture of tax treatment you must:

- Be age 59 ½ AND

- Had the account open for 5 years or more.

Randolph is going to be age 60 when he retires, so he made one of two requirements. He also mentions that he has ⅓ of his account balance in the ROTH so we can presume this has been open for 5+ years.

What to use first: Traditional or ROTH TSP funds?

Build a retirement timeline to determine when you should use your Traditional TSP funds vs. the ROTH TSP funds.

———————————————————————————————————————————————————–

Age 60 Age 100

Where on this timeline do you start receiving income and what portion of that income is taxable?

Are taxes going to go down or are taxes going to go up in the future? Forget about your income for a moment and just think about the direction of taxes, are they going to go up or are they going to go down?

If you, like most people think that they’re going to go up in the future, then now we need to think about whether or not it makes more sense to pay taxes today when you know what the rate is and your income is vs. in the future when you do not know.

Tax planning in retirement, looking at decades at a time is a critical component of your retirement planning.

Additionally, if we think taxes are going to go up in the future, we may want to delay taking funds out of a tax-free account for as long as possible and continue to allow these funds to potentially grow.

If you’re a long-time follower of Plan Your Federal Retirement on our podcast, website, or youtube channels then you already know that we are adamant at our firm about the 5-year rule.

Money that you need to spend/have in the next 5 years does not belong in the stock market.

It is not a matter of “if” the stock market has a correction but “when” the stock market corrects. If life goes as it should, you could be retired for 40+ years. During that time span, the markets are going to continue to be volatile and experience growth and contractions. That is why it is so important to know before a contraction happens, what is your plan.

We strongly recommend that you have a financial plan that accounts for how and when you need to spend money from your investments and what your strategy is going to be when markets correct.

Randolph asked a great question and brought to light just how many moving components you have as a Federal Employee to consider. If you want answers to potentially maximize your benefits and develop a financial plan that works with your benefits in mind, make sure that you reach out to our firm.