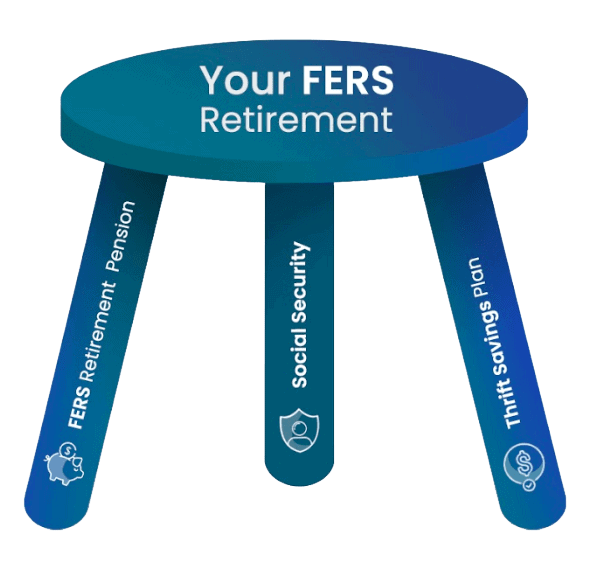

When we talk about your FERS Retirement, we’re really talking about several different benefits. FERS (Federal Employees Retirement System) has three main components:

- Basic FERS Retirement Pension

- Social Security

- Thrift Savings Plan (TSP)

Your FERS pension and Social Security will be fixed dollar amounts. But the money you get from your TSP will depend on how much you contributed and how well you managed the money.

As a FERS, you have a chance to take a more active role in managing your own retirement than CSRS do. But, that means you need to stay up-to-date on your benefits.

First – let’s talk about FERS Retirement eligibility rules. Then we’ll take a closer look at each leg of your FERS Retirement …

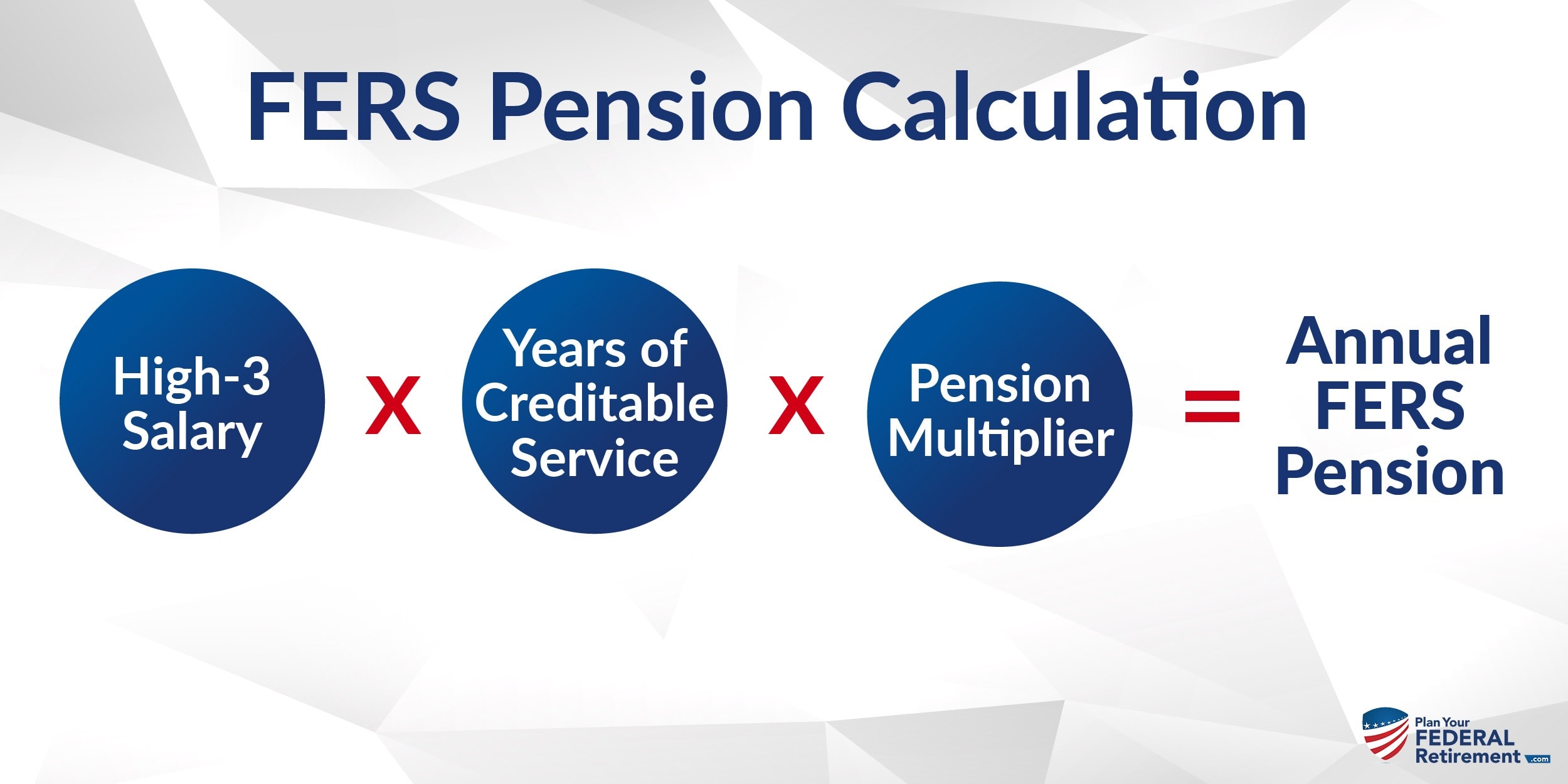

FERS Pension Calculation

The calculation looks simple. But the complexity comes in how you calculate your High-3 Salary, and what really counts towards your Years of Creditable Service.

Click here to learn more about how each part of your pension formula is calculated and see examples of FERS pension calculations.

![live127123 [Converted] 1-01](https://plan-your-federal-retirement.com/wp-content/uploads/elementor/thumbs/live127123-Converted-1-01-qlhfxt1jl8nai44kz1xk5u4shejeynh2t7i0txhx7c.png "live127123 [Converted] 1-01")